Financial emergencies often force people to make difficult decisions under immense pressure and stress. Reaching for a credit card might seem like the most convenient solution when facing unexpected expenses. Certain purchases and payments can transform a temporary crisis into a permanent cycle of unmanageable debt. Understanding which transactions to avoid is absolutely crucial for protecting your long term financial health.

Bail Bonds

Paying for bail with a credit card might seem like a quick solution but it often carries astronomical fees from the bonding agency. Credit card companies generally treat these transactions as cash advances which immediately begin accumulating interest at a much higher rate. The compounded debt can quickly become unmanageable and create a long term financial burden far worse than the original fine. Individuals facing legal trouble should explore alternative options like borrowing from family or negotiating a payment plan with the court directly.

Mortgage Payments

Using credit to pay for your primary residence usually involves third party processing services that charge substantial convenience fees. The combination of these processing fees and standard credit card interest rates makes this an incredibly expensive way to maintain your housing. Missing the subsequent credit card payment can severely damage your credit score while still leaving your housing situation vulnerable. Homeowners experiencing financial hardship are better served by contacting their lender to discuss forbearance programs or temporary modification options.

Student Loans

Most federal loan servicers strictly prohibit direct credit card payments to prevent borrowers from transferring lower interest debt to high interest accounts. Using third party platforms to bypass this restriction adds significant transaction fees that negate any potential rewards points or benefits. Transitioning student debt to a credit card also strips away vital borrower protections like income driven repayment plans and deferment options. Borrowers struggling with monthly obligations should instead apply for federal hardship programs or consider refinancing through traditional banking channels.

Income Taxes

The Internal Revenue Service utilizes third party processors that charge a percentage based fee for all credit card tax payments. This processing fee entirely erodes the value of any cash back or travel rewards you might earn from the transaction. Financing your tax burden through a credit card also exposes you to compounding interest rates that quickly inflate your total tax liability. Taxpayers unable to pay their balance in full should apply for an official installment agreement directly through the government website.

Stock Market Investments

Funding investment accounts with a credit card breaks the fundamental rule of not gambling with borrowed money. Brokerages typically classify these deposits as cash advances which instantly trigger hefty fees and exorbitant interest rates. The stock market is inherently volatile and any potential gains will almost certainly be eclipsed by the accumulating debt charges. Investors must rely strictly on available liquid cash to build their portfolios safely and responsibly.

Cryptocurrency Purchases

Buying digital currency on credit introduces severe financial risk due to the extreme volatility of these decentralized markets. Major exchanges and credit issuers classify these transactions as cash advances subject to immediate high interest accrual. A sudden drop in the asset value leaves the purchaser holding a massive debt without the means to pay it off. Financial experts universally advise using only disposable income for any speculative digital asset acquisitions.

Casino Chips

Withdrawing funds on a credit card at a gaming establishment is universally considered a dangerous financial maneuver. These transactions immediately incur cash advance fees and begin accruing interest without any grace period. The odds inherently favor the house which means the borrowed funds will likely be lost alongside the heavy interest burden. Individuals should strictly bring predetermined amounts of cash to avoid creating long lasting debt from a short entertainment experience.

Lottery Tickets

Many states legally prohibit retailers from accepting credit cards for lottery purchases to protect consumers from gambling debts. In locations where it is allowed the transaction operates as a cash advance with immediate financial penalties. The statistical improbability of winning means consumers are essentially paying premium interest rates for worthless pieces of paper. Buying chances to win money should only ever involve spare cash that you are completely prepared to lose.

Car Payments

Auto lenders rarely accept direct credit card payments because the merchant processing fees would cut into their profit margins. Utilizing third party payment services to facilitate the transaction adds expensive surcharges to your monthly transportation budget. Shifting secured auto debt onto an unsecured high interest credit line creates a dangerous cycle of compounding financial liability. Drivers facing repossession should immediately contact their financing company to discuss deferment rather than relying on plastic.

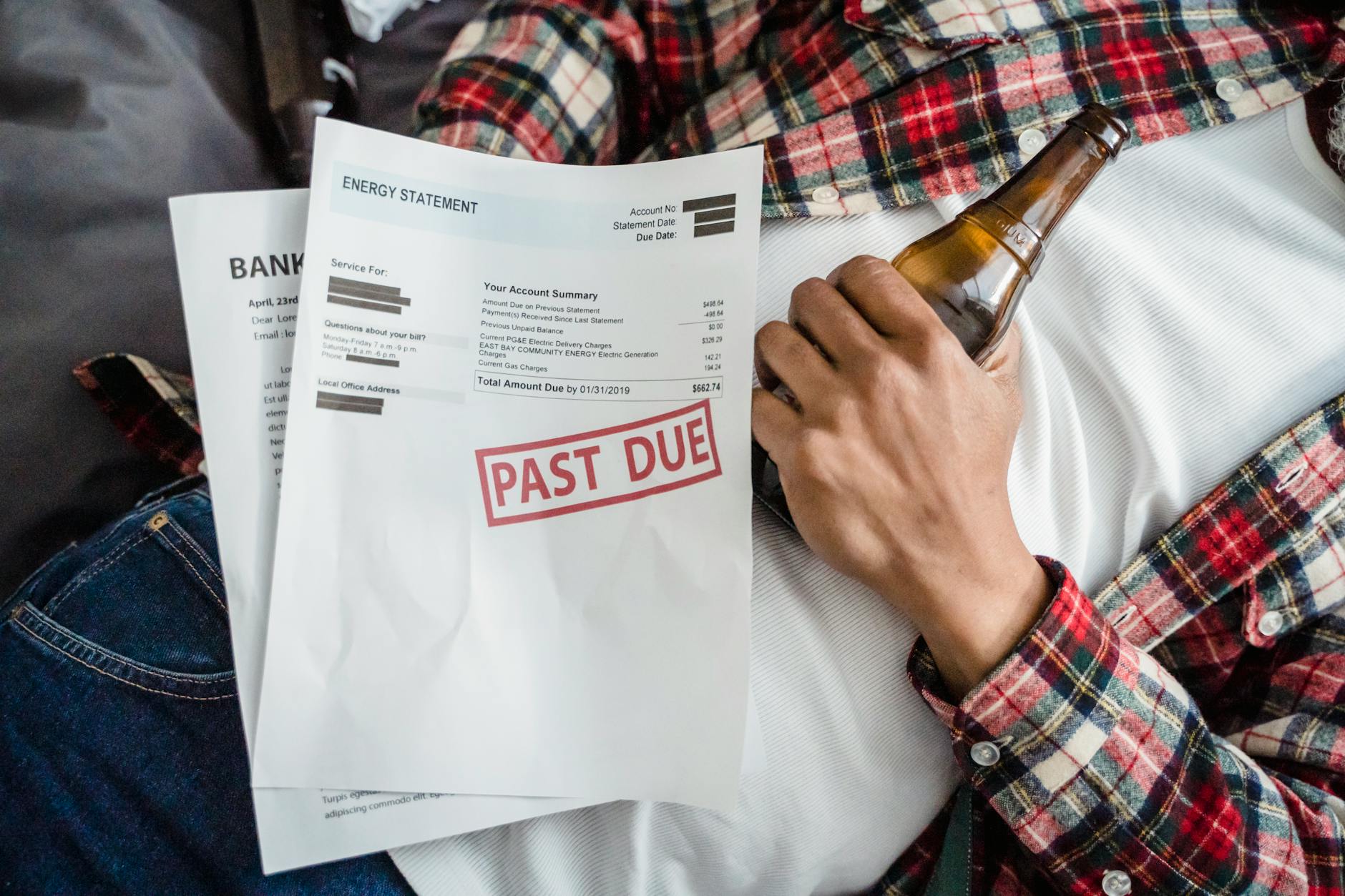

Medical Bills

Hospitals and clinics often offer zero interest payment plans that are vastly superior to standard credit card terms. Placing a massive emergency room bill on your card converts a manageable medical debt into a rapidly growing financial crisis. Credit bureaus also treat medical debt more leniently than consumer credit card debt when calculating your credit score. Patients should always negotiate directly with the billing department to establish an affordable monthly schedule before turning to credit.

Down Payments

Using a credit card to secure a home or vehicle creates an immediate red flag for underwriting departments and lenders. This action significantly alters your debt to income ratio and will likely result in a denied mortgage or auto loan application. The massive balance will also incur heavy interest charges that make the underlying asset far more expensive than its actual value. Buyers must diligently save liquid cash for these initial payments to demonstrate financial stability to potential creditors.

College Tuition

Universities routinely charge massive convenience fees for tuition payments made with credit cards to cover their processing costs. These administrative fees easily add hundreds of dollars to an already expensive educational investment. Financing education at standard credit card interest rates is mathematically disastrous compared to traditional subsidized student loans. Families should exhaust all federal aid and private educational loans before ever considering putting a semester on plastic.

Alimony Payments

Fulfilling court ordered spousal support through a credit card requires using expensive third party services that inflate the total cost. Transitioning this legal obligation into consumer debt adds compound interest to a payment you already struggle to afford. Missed credit card payments will ruin your financial standing while failing to solve the underlying cash flow problem. Individuals unable to meet their alimony requirements must petition the court for a formal modification instead of creating toxic debt.

Child Support

State agencies process child support payments through specialized portals that tack on significant transaction fees for credit usage. The accumulation of high interest on these recurring payments creates an unsustainable financial burden over time. Falling behind on the credit card balance jeopardizes your credit score and threatens your broader financial stability. Parents experiencing temporary unemployment or hardship should file for an official adjustment through the family court system immediately.

Bankruptcy Fees

Paying legal fees for a bankruptcy filing with a credit card is legally problematic and highly scrutinized by the courts. Judges can dismiss the bankruptcy entirely if they suspect the debtor took on new credit card debt without the intention of repaying it. This desperate measure often complicates the legal proceedings and adds unnecessary stress to an already difficult process. Debtors must use cash or rely on family members to cover the necessary legal costs associated with filing for financial relief.

Funeral Expenses

Grieving families often make rushed financial decisions and putting funeral costs on a credit card is a common mistake. The emotional toll of a loss is only amplified when a massive high interest bill arrives weeks later. Many funeral homes offer direct payment plans or work with specialized lenders providing more reasonable terms. It is essential to choose affordable end of life arrangements that do not compromise the financial security of the surviving relatives.

Traffic Tickets

Municipalities utilize independent processing vendors that add nonrefundable service charges to all credit card transactions for moving violations. Paying a substantial fine on credit turns a simple legal penalty into an expensive long term financial obligation. The combined cost of the ticket plus processing fees and compound interest easily doubles the original penalty. Drivers should appear in court to request a structured payment plan or perform community service to satisfy the debt.

Legal Fees

Retaining an attorney with a credit card forces you to pay double digit interest on incredibly expensive billable hours. Law firms often pass merchant processing fees directly onto the client which further increases the total cost of representation. Ongoing legal battles can quickly exhaust your available credit limit and leave you without resources for everyday necessities. Clients should negotiate a flat fee structure or a monthly retainer plan directly with the law firm to avoid consumer debt.

Small Business Capital

Funding a startup venture with personal credit cards mixes business liabilities with your private financial standing. High consumer interest rates devour early profits and severely restrict the cash flow necessary for business growth. A failed enterprise will leave you personally responsible for the entire debt and completely destroy your individual credit score. Entrepreneurs must seek out proper commercial loans or secure venture capital to fund their business operations safely.

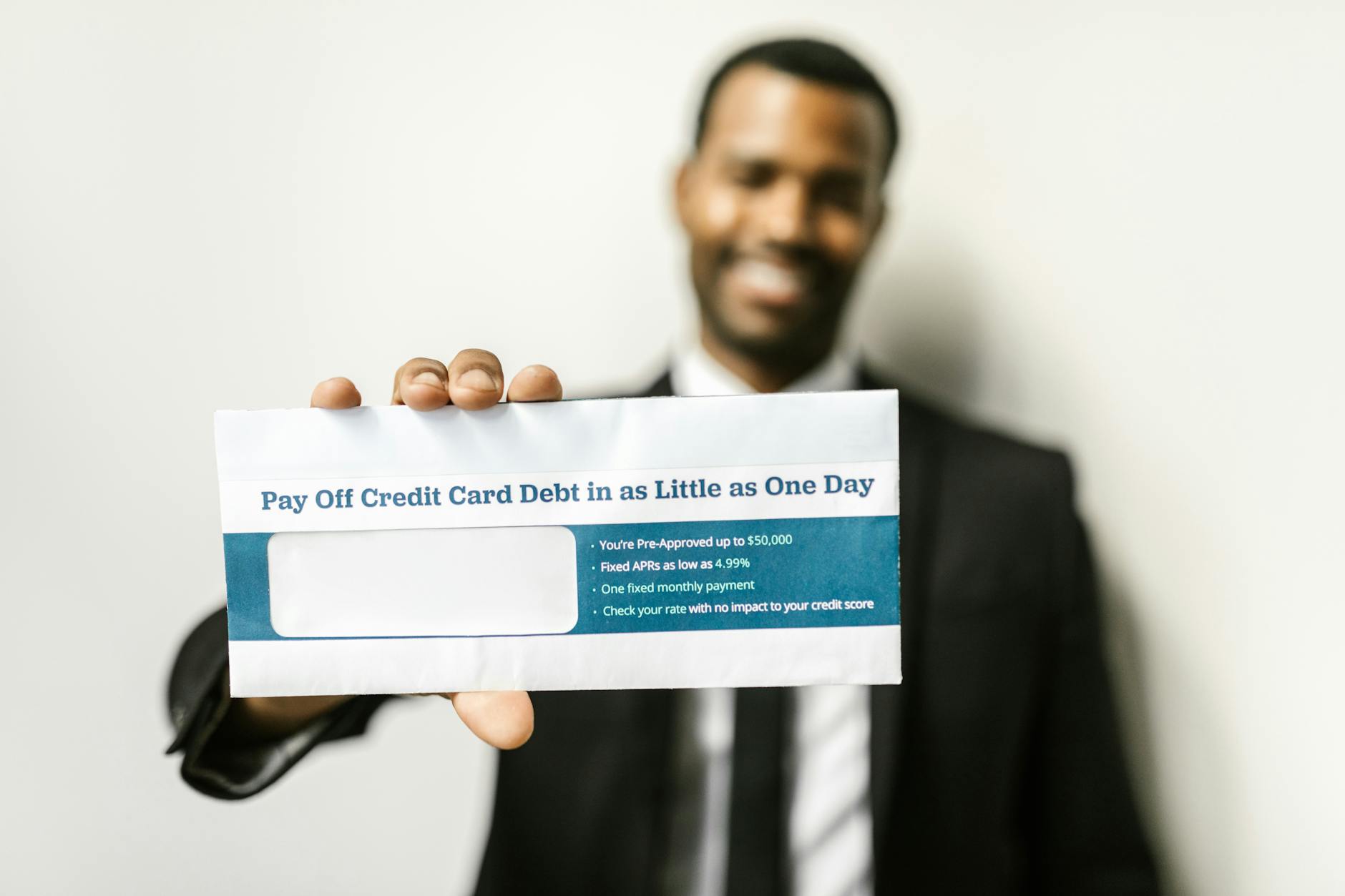

Payday Loan Payoffs

Shifting a predatory payday loan onto a credit card merely trades one form of toxic debt for another. While the credit card interest rate might be marginally lower the balance still grows at an alarming pace. This strategy fails to address the underlying budget deficit that caused the initial need for the payday loan. Consumers should seek assistance from nonprofit credit counseling agencies to establish a sustainable debt management plan instead.

Personal Loan Repayments

Using a credit card to satisfy a personal loan installment requires cash advance maneuvers that trigger exorbitant fees. This approach essentially creates a debt pyramid where high interest consumer credit pays off fixed installment debt. The borrower ends up paying interest twice on the exact same principal amount over an extended period. Contacting the original lender to request a temporary forbearance is always preferable to initiating a cash advance.

Real Estate Taxes

Local tax authorities employ processing companies that charge a hefty premium for accepting credit card property tax payments. The extra expense easily negates the value of any rewards points and adds unnecessary cost to property ownership. Rolling annual property taxes into high interest revolving debt makes it increasingly difficult to afford the home over time. Homeowners should utilize an escrow account through their mortgage servicer to save for tax obligations efficiently.

Wedding Expenses

Financing a lavish wedding ceremony on credit cards ensures a newlywed couple begins their marriage buried under financial stress. The interest charges on catering and venue rentals will linger for years after the celebration has ended. Financial counselors consistently cite consumer debt as a primary catalyst for marital arguments and eventual divorce. Couples must strictly adhere to a cash budget and plan a celebration they can afford without borrowing money.

Engagement Rings

Purchasing expensive jewelry on a standard credit card exposes the buyer to incredibly steep retail interest rates. The compound interest dramatically inflates the true cost of the ring and creates a heavy burden right before a wedding. Many jewelers offer zero percent promotional financing that is far more sensible than using a traditional revolving credit line. Saving up to buy the ring outright remains the safest way to make this important symbolic investment.

Elective Surgery

Putting cosmetic procedures on a credit card transforms an optional enhancement into a severe financial liability. Medical financing companies typically offer dedicated loans with much more favorable terms than regular credit issuers. High interest debt associated with elective procedures often causes immense psychological stress during the vital recovery period. Patients should delay their cosmetic goals until they have saved enough liquid cash to cover the entire procedure comfortably.

Please share your thoughts on managing financial emergencies and let us know which of these credit card mistakes you consider the most dangerous in the comments.