Your credit score is one of the most powerful numbers attached to your financial identity, influencing everything from loan approvals to rental applications. A strong score takes years of disciplined behavior to build, yet certain everyday habits can quietly erode it far faster than most people expect. Understanding what damages your score is the first step toward protecting the financial reputation you have worked hard to establish. These 25 habits are among the most common and most destructive patterns seen by financial experts across the country.

Missing Payment Deadlines

Payment history is the single largest factor in most credit scoring models, typically accounting for around 35 percent of your total score. Even one late payment can cause a noticeable drop, and the damage becomes more severe the longer the account remains unpaid. Creditors generally report a payment as late once it has passed 30 days beyond the due date. Setting up automatic payments or calendar reminders is one of the simplest ways to avoid this costly mistake. Consistent on-time payments are the foundation of a healthy credit profile.

Maxing Out Credit Cards

Credit utilization measures how much of your available revolving credit you are actively using at any given time. Carrying balances close to your credit limits signals financial stress to lenders and scoring algorithms alike. Most financial experts recommend keeping utilization below 30 percent across all cards combined. Accounts that are consistently near their limits can drag your score down significantly even if payments are made on time. Paying down balances rather than simply making minimum payments is the most effective way to improve this ratio.

Closing Old Credit Accounts

The length of your credit history plays a meaningful role in determining your overall score. When you close an old account, you remove years of positive payment history and reduce your total available credit in one move. This can cause your utilization rate to spike overnight if you are carrying balances on other cards. Older accounts that are rarely used are often better left open with a small occasional purchase to keep them active. The age of your oldest account and the average age of all accounts both factor into how your history is evaluated.

Applying for Too Much Credit at Once

Every time you formally apply for a new line of credit, the lender performs a hard inquiry on your credit report. A single hard inquiry typically causes only a minor dip, but multiple applications within a short period can add up quickly. Lenders interpret a flurry of applications as a sign that a borrower may be in financial difficulty or taking on more debt than they can manage. Shopping for rates on mortgages or auto loans is generally treated more leniently within a focused window, but credit card applications do not receive the same grouping benefit. Spacing out applications and only seeking new credit when truly necessary helps protect your score over time.

Ignoring Your Credit Report

Millions of consumers have never reviewed their credit report, leaving errors and fraudulent accounts undetected for years. Inaccurate information such as a wrongly reported late payment or an account that does not belong to you can suppress your score without your knowledge. Each of the three major credit bureaus is required to provide a free report annually upon request. Reviewing your report regularly allows you to catch discrepancies early and file disputes before the damage compounds. Proactive monitoring is one of the most underutilized tools available to everyday consumers.

Paying Only the Minimum Balance

While making minimum payments does technically satisfy your payment obligation, it keeps balances high and utilization elevated for extended periods. Minimum payments are structured in a way that maximizes the amount of interest paid over time, keeping borrowers in a cycle of revolving debt. High outstanding balances relative to credit limits continue to drag on your score month after month. The psychological comfort of meeting the minimum can mask the long-term financial and credit damage being done. Paying as much above the minimum as possible accelerates debt reduction and improves your utilization ratio.

Using Credit Cards for Cash Advances

Cash advances are treated differently from standard purchases and often carry immediate fees along with higher interest rates. Unlike regular transactions, interest on cash advances typically begins accruing the moment the funds are withdrawn with no grace period. Frequent use of this feature can signal to lenders that a borrower is struggling with cash flow. While cash advances do not directly label themselves on your credit report, the increased balance activity raises utilization. This habit is one of the more expensive and credit-damaging ways to access short-term funds.

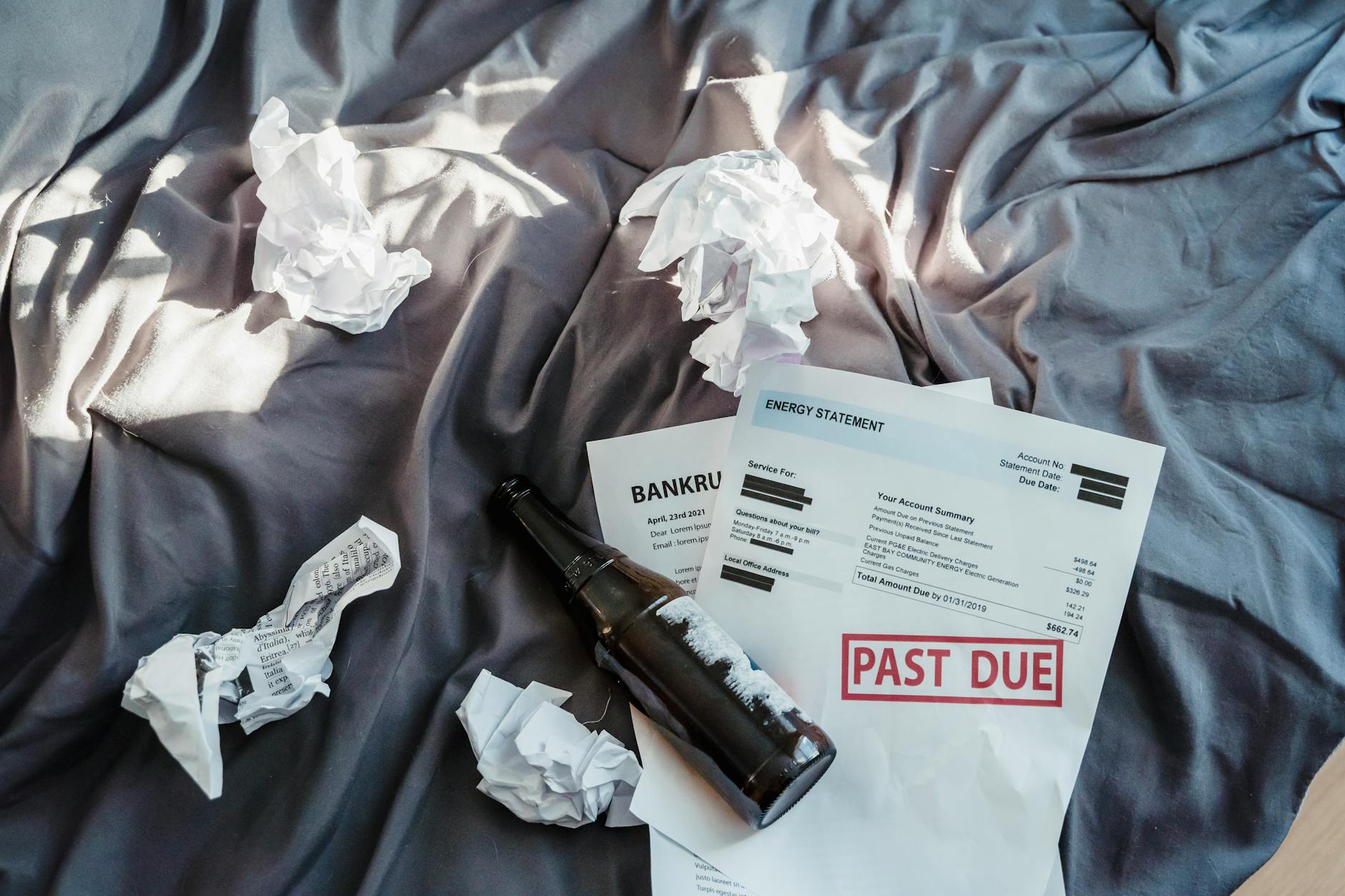

Letting Bills Go to Collections

When an unpaid debt is transferred to a collection agency, the impact on your credit score can be severe and long-lasting. A collection account can remain on your credit report for up to seven years from the date of the original delinquency. Even after the debt is paid or settled, the collection entry often remains visible to future lenders. Medical bills, utility accounts, and subscription services are among the most common types of accounts that slip into collections unnoticed. Addressing overdue accounts before they are sold to collectors is far less damaging than dealing with the aftermath.

Defaulting on Loans

Loan default occurs when a borrower fails to make required payments for an extended period and the lender declares the debt in default status. This event is recorded on your credit report and represents one of the most serious negative marks possible. Defaults on student loans, personal loans, and auto loans each carry significant consequences and can remain on your report for years. Lenders reviewing your file in the future will see a default as a major red flag when evaluating whether to extend new credit. Contacting a lender proactively to discuss hardship options before reaching default status can sometimes prevent the worst outcomes.

Filing for Bankruptcy

Bankruptcy is a legal process designed to help individuals unable to repay their debts, but it comes with serious long-term credit consequences. A Chapter 7 bankruptcy can remain on a credit report for up to ten years, while Chapter 13 typically stays for seven. During that period, accessing new credit becomes significantly more difficult and more expensive in terms of interest rates. Lenders view a bankruptcy filing as a fundamental breakdown in a borrower’s ability to manage financial obligations. While bankruptcy can offer a fresh start, the credit rebuilding process that follows requires years of sustained effort.

Carrying High Balances Month to Month

Allowing high balances to sit on credit cards without actively reducing them keeps your utilization rate persistently elevated. Scoring models evaluate your balances at the time they are reported, typically around the closing date of your billing cycle. Even if you intend to pay off the balance soon, a high reported balance is what affects your score at that snapshot in time. Borrowers who consistently carry large balances are viewed as higher risk by both scoring algorithms and human underwriters. Making payments before the statement closing date rather than after is a strategy used to keep reported balances low.

Opening Too Many New Accounts

Each new account you open lowers the average age of your credit history and contributes an additional hard inquiry to your report. Opening multiple accounts in a short period can create the appearance of financial instability or desperation for credit. New accounts also lack the positive payment history that older accounts carry, reducing the overall quality of your credit file. Lenders extending credit in the future will see a high concentration of recently opened accounts as a risk indicator. Building credit slowly and deliberately through a manageable number of accounts tends to produce better long-term results.

Skipping Rent or Utility Payments

While traditional rent payments have historically not appeared on credit reports automatically, many landlords and property managers now report to credit bureaus through third-party services. Utility accounts sent to collections after nonpayment have always had the potential to appear negatively on a credit report. Some newer credit scoring models incorporate rent and utility payment history into their calculations, expanding the impact of these habits. Falling behind on housing costs can create a cascade of financial stress that affects multiple credit-related accounts simultaneously. Treating rent and utilities with the same urgency as credit card payments is increasingly important in the modern credit landscape.

Not Diversifying Credit Types

Credit mix refers to the variety of credit accounts you hold, including revolving credit like cards and installment credit like loans. Lenders and scoring models generally view borrowers more favorably when they can demonstrate responsible management of multiple types of credit. A credit profile consisting entirely of one type of account may be seen as less robust than one that includes a mix. This does not mean opening unnecessary accounts purely for diversity, but rather allowing natural financial needs to create a varied mix over time. Installment loans, mortgages, and revolving accounts each tell a different story about a borrower’s financial behavior.

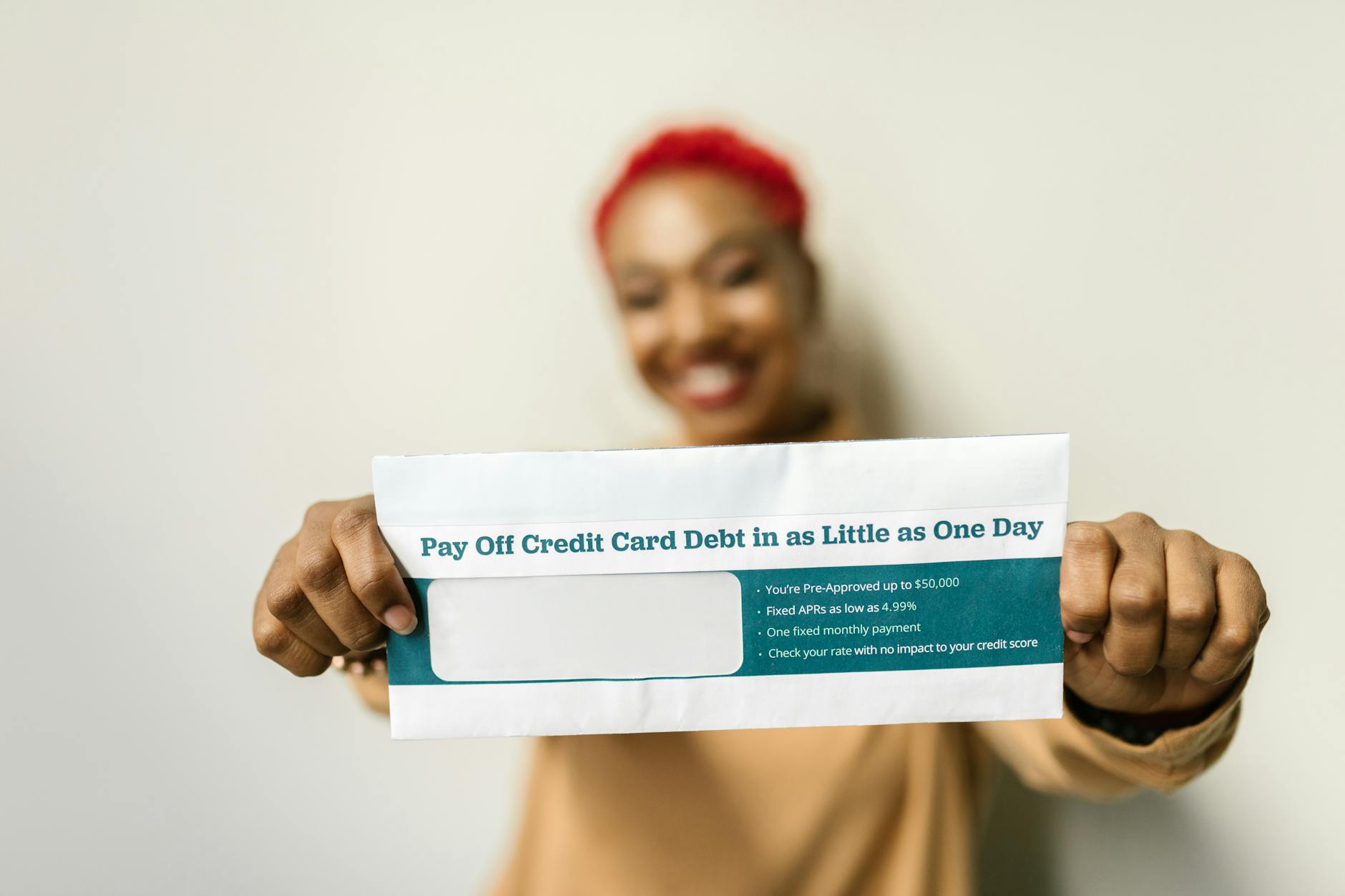

Falling for Credit Repair Scams

Companies that promise to quickly erase negative items from your credit report often use misleading or outright fraudulent tactics. In some cases, their methods involve disputing accurate information or creating a new credit identity, both of which can have legal consequences for the consumer. Paying fees to a credit repair company for services you can legally perform yourself is a common and costly mistake. Legitimate negative information remains on your credit report regardless of what a third-party company claims it can do. Understanding your rights under consumer protection laws is a far more effective and safe approach to managing your credit health.

Overlooking Fraudulent Activity

Identity theft can introduce fraudulent accounts, late payments, and collections into your credit file without your awareness. Victims of identity theft sometimes discover the damage only when they are denied credit for a major purchase. The process of resolving fraudulent accounts is time-consuming and requires filing disputes, police reports, and in some cases fraud alerts with the credit bureaus. The longer fraudulent activity goes undetected, the more extensive the damage tends to become. Regular monitoring of your credit report and account statements is the most reliable way to catch unauthorized activity early.

Cancelling Cards After Paying Them Off

Paying off a credit card is a financial achievement, but immediately closing the account can undo some of the credit benefit. Closing a paid-off card reduces your total available credit and increases your overall utilization if balances remain on other accounts. If the card is one of your oldest accounts, closing it also shortens the average age of your credit history. Keeping a paid-off card open and occasionally making small purchases to maintain activity preserves both the credit history and the available limit. The card does not need to carry a balance to contribute positively to your credit profile.

Making Late Mortgage Payments

Mortgage payments carry particular weight in credit scoring because they represent the largest and most serious financial obligation for most borrowers. A single late mortgage payment can cause a more significant drop in your score than a late credit card payment of the same delinquency period. Mortgage lenders report payment behavior consistently to all three major credit bureaus, meaning the record is comprehensive and widely visible. Multiple late mortgage payments within a short period can trigger further consequences including the lender initiating collection procedures. Prioritizing mortgage payments above other financial obligations is standard advice from credit counselors and financial advisors alike.

Neglecting Student Loan Payments

Student loan debt represents a significant portion of overall consumer debt in many countries, and missed payments carry real credit consequences. Federal and private student loans both report payment history to the credit bureaus, making consistent on-time payments critical. Borrowers who ignore their student loans after graduating often discover that the damage to their credit profile makes other financial goals like homeownership far more difficult. Income-driven repayment plans and deferment options exist for federal loans specifically to help borrowers avoid default. Proactively communicating with a loan servicer about payment difficulties is far less damaging than allowing payments to lapse without contact.

Overspending During the Holidays

Seasonal spending spikes, particularly during the winter holidays, are one of the most common causes of sudden increases in credit card balances. Consumers who charge large gift purchases and travel expenses often carry those balances well into the following year. This temporary but significant rise in utilization can cause a noticeable credit score decline that lingers for months. Retailers and credit card companies frequently promote limited-time offers and new card incentives during the holiday season, encouraging applications that generate additional hard inquiries. Creating a holiday budget and relying on cash or debit for discretionary spending helps avoid the post-season credit hangover.

Ignoring Medical Bills

Medical billing is one of the most confusing areas of personal finance, and many consumers are unaware that unpaid medical bills can affect their credit. While recent changes to credit reporting rules have reduced the weight of some medical debt, larger unpaid balances can still reach collections and appear on your report. Billing errors in the healthcare system are common, and patients who do not review their statements may end up with incorrect debt attributed to them. Hospitals and medical providers frequently offer payment plans or financial assistance programs that can prevent accounts from being sent to collections. Addressing medical bills promptly and requesting itemized statements to check for errors is an important financial habit.

Mixing Business and Personal Credit

Business owners who use personal credit cards for business expenses risk increasing their personal utilization rates with charges that may not be immediately repaid. Commingling business and personal finances also makes it harder to track spending, dispute errors, and manage tax obligations. Personal guarantees on business lines of credit or loans mean that business financial problems can directly damage the owner’s personal credit score. Establishing a separate business credit profile not only protects personal credit but also builds creditworthiness for the business as a standalone entity. Financial advisors consistently recommend separating these two categories from the earliest stages of business operation.

Failing to Dispute Errors

Errors on credit reports are more common than most consumers realize, affecting a significant percentage of all reports reviewed by consumer advocacy groups. Common errors include duplicate accounts, incorrect personal information, accounts belonging to someone with a similar name, and payments marked late despite being submitted on time. Credit bureaus are legally required to investigate disputes and correct or remove inaccurate information within a set timeframe. Failing to dispute errors means allowing inaccurate negative information to suppress your score indefinitely. The dispute process can be initiated directly through each bureau’s website and does not require the assistance of a paid service.

Sharing Account Access Without Boundaries

Adding an authorized user to your account or co-signing a loan for someone else ties your credit to their financial behavior. If the person you have extended access to misses payments or maxes out the account, the consequences appear on your credit report alongside theirs. Co-signing is particularly risky because you become equally responsible for the debt in the eyes of the lender. Many borrowers discover the damage only after a relationship has broken down or the other party has stopped communicating. Any decision to share credit access should be treated with the same seriousness as taking on the financial obligation independently.

Living Beyond Your Means

Spending consistently more than your income allows creates a cycle of debt accumulation that steadily erodes your credit health. Relying on credit cards to fund a lifestyle that exceeds your actual earnings leads to growing balances and rising utilization over time. This pattern eventually makes it difficult to meet minimum payments let alone make meaningful progress on reducing principal. Financial stress from overspending often leads to prioritizing some bills over others, creating late payments across multiple accounts. Aligning spending habits with actual income is the most sustainable and credit-protective financial strategy available to any consumer.

Share your own experiences with credit habits or questions you have about protecting your score in the comments.