Walking into a used car dealership without insider knowledge is one of the most financially costly mistakes a consumer can make. The entire sales environment is engineered from the layout of the lot to the language of the contract to extract the maximum amount of money from every single buyer. Dealerships operate on information asymmetry and the moment a customer closes that gap the dynamic shifts entirely in their favor. These are the secrets the industry counts on you never discovering.

Emotional Anchoring

The first vehicle a salesperson walks you toward is almost never chosen by accident and is typically priced above your stated budget to establish a high psychological reference point. Once a buyer has mentally engaged with a more expensive vehicle the subsequent options presented feel like reasonable compromises even when they still exceed the original budget. This anchoring technique is borrowed directly from behavioral economics and is applied consciously in dealership sales training. Recognizing that the opening vehicle is a positioning tool rather than a genuine recommendation immediately disrupts the intended effect.

Spot Delivery

A financing practice known as spot delivery allows a dealership to hand over a vehicle before financing has been formally approved by a lender allowing the buyer to drive away feeling the deal is complete. Days or weeks later the buyer receives a call informing them that the original financing terms could not be secured and that a higher interest rate or larger down payment is now required. By this point the buyer has emotionally bonded with the vehicle registered it and in many cases traded in their previous car creating enormous leverage for the dealership to renegotiate from a position of strength. This practice is legal in many jurisdictions and is specifically designed to exploit the psychological commitment that follows taking possession.

Trade-In Timing

Revealing that you have a trade-in before negotiating the purchase price of the new vehicle gives the dealership a critical tool for obscuring profitability across both transactions simultaneously. A salesperson can appear to offer a generous trade-in value while quietly adjusting the purchase price upward by an equivalent or greater amount making the overall deal less favorable than it appears. The two transactions should always be negotiated completely separately with the purchase price agreed upon in writing before any trade-in conversation begins. Experienced buyers frequently sell their existing vehicle privately to remove this variable entirely from the dealership negotiation.

Monthly Payment Focus

Steering a buyer’s attention toward the monthly payment rather than the total purchase price is the single most profitable conversational pivot a dealership salesperson can execute. Extending the loan term from four years to seven years can make a vehicle that is thousands of dollars overpriced appear affordable on a monthly basis while dramatically increasing the total cost through accumulated interest. A dealership can manipulate the monthly figure by adjusting any combination of price term and interest rate making the payment an almost meaningless metric for evaluating the actual cost of the deal. Total out-of-pocket cost over the life of the loan is the only number that accurately represents what a vehicle will cost.

Dealer Add-Ons

Items appearing on the final purchase contract under labels including paint protection fabric guard nitrogen-filled tires VIN etching and window tinting are almost universally marked up by several hundred to over a thousand percent relative to their actual cost or market value. These additions are frequently presented as already installed on the vehicle making buyers feel obligated to pay for something they never agreed to purchase. Each item on a dealer add-on list is negotiable or removable and the buyer is under no legal obligation to accept or pay for any pre-installed accessory they did not specifically request. Reviewing the itemized contract before signing rather than at the point of signature pressure is the most effective way to identify and remove these charges.

Finance Office Upsells

The finance and insurance office which buyers enter after agreeing on a vehicle price is a separate and highly profitable revenue center designed to extract additional money from buyers who believe the negotiation is already complete. Extended warranties GAP insurance credit life insurance tire and wheel protection and prepaid maintenance packages are all sold in this room at significant margins above their actual value or what the same products cost elsewhere. The finance manager is a trained specialist whose primary function is revenue generation not customer service and the relaxed post-deal atmosphere of the room is a deliberate design choice. Every product offered in the finance office should be researched independently and if desired purchased separately before the dealership visit.

Certified Pre-Owned Illusion

The certified pre-owned designation commands a significant price premium over a non-certified equivalent vehicle but the standards and inspection depth behind different manufacturer certification programs vary enormously from one brand to another. Some programs involve comprehensive multi-point inspections with meaningful warranty coverage while others represent a basic visual check with a largely cosmetic certification label applied to justify the premium. The certification does not guarantee that all existing issues were identified or disclosed and it does not replace the independent inspection of a trusted mechanic before purchase. Understanding exactly what a specific manufacturer’s certification program covers and comparing the premium charged against actual warranty terms is the only way to evaluate whether the designation adds genuine value.

Lowball Internet Price

Advertised online prices for used vehicles frequently include deductions for incentives the buyer may not qualify for or dealer discount conditions that require specific financing or trade-in arrangements to access. When a buyer arrives at the dealership having researched the internet price the actual out-the-door figure often climbs significantly through the addition of fees accessories and financing conditions not disclosed in the advertisement. The gap between the advertised price and the real transaction price is a calculated strategy that drives foot traffic to the dealership by presenting an artificially attractive entry point. Requesting the complete out-the-door price including all fees taxes and charges in writing before visiting a dealership eliminates the most common form of this bait-and-switch dynamic.

Dealer Fees

Documentation fees administrative fees dealer preparation fees and a wide variety of similarly labeled charges that appear on purchase contracts represent pure profit for the dealership and have no corresponding service of equivalent value delivered to the buyer. These fees vary enormously between dealerships for identical services and in many regions face no regulatory cap making them a direct function of what the market will tolerate. While some fees are presented as mandatory and non-negotiable buyers who push back on excessive fee amounts frequently find them reduced or partially credited particularly when demonstrating awareness of the going rate in the local market. Comparing the fee structures of competing dealerships before entering negotiations provides the reference point needed to challenge inflated charges with credibility.

The Four-Square

A physical or digital worksheet known in the industry as the four-square divides the deal into four boxes representing purchase price trade-in value down payment and monthly payment and is used to manage buyer attention and obscure the true cost of the transaction. By shifting numbers between boxes the salesperson can make the overall deal appear favorable in whichever dimension the buyer seems most focused on while protecting profitability in the areas receiving less scrutiny. The four-square is specifically designed to prevent buyers from clearly seeing the total cost of the transaction and to generate the psychological impression of winning concessions. Refusing to negotiate using the four-square format and insisting on discussing each element as a separate line item removes the tool’s primary advantage.

Rushed Signing

The pace at which dealership contracts are presented for signature is rarely accidental with salespeople trained to maintain forward momentum through the paperwork process in a way that discourages careful reading. Buyers who ask to slow down review each page independently and read every clause before signing are statistically far less likely to agree to unfavorable terms hidden within standard contract language. Taking the contract home to review or requesting a digital copy to examine without time pressure is a right that buyers hold and a practice that dealerships are systematically trained to discourage. The urgency projected during the signing process is a manufactured condition not a genuine deadline.

Vehicle History Gaps

A vehicle history report from services such as Carfax or AutoCheck provides documented records of registered accidents ownership history and title issues but has significant and well-known gaps that dealerships understand and buyers frequently do not. Accidents that were repaired without an insurance claim cash-funded repairs at shops that do not report to history databases and damage that occurred in jurisdictions with incomplete reporting coverage all fall below the radar of standard history reports. A clean vehicle history report is therefore a baseline requirement rather than a clearance and an independent inspection by a qualified mechanic remains essential regardless of what the report shows. Framing a clean history report as comprehensive reassurance is a consistent dealership practice that leads buyers to skip the inspection step.

Salvage Title Washing

A vehicle that has received a salvage title following significant damage can in some jurisdictions have that title designation obscured or reclassified through a series of ownership transfers across state lines a practice known as title washing. The resulting vehicle enters the market with a clean or rebuilt title that does not fully reflect its damage history allowing it to be sold at a price that does not account for the significant reduction in structural integrity safety and resale value associated with major prior damage. Checking a vehicle’s history across multiple databases and having the body and frame independently inspected for repair evidence are the most reliable defenses against purchasing a washed title vehicle unknowingly. VIN checks through the National Insurance Crime Bureau database provide an additional layer of investigation beyond standard history reports.

Odometer Discrepancies

Digital odometers are not immune to tampering and while modern tampering is more technically demanding than the mechanical rollback of older vehicles it remains a documented fraud pattern in the used vehicle market particularly for high-mileage vehicles being prepared for retail sale. Comparing the stated mileage against wear indicators including pedal rubber steering wheel wear seat bolster condition and door sill scuffing provides a cross-reference that a tampered odometer cannot consistently support. Service records that reference mileage at prior visits provide a documented timeline that can expose inconsistencies a tampered digital display would otherwise conceal. Any significant mismatch between odometer reading and visible wear profile warrants investigation before proceeding with a purchase.

Auction Pipeline

A significant proportion of the used vehicle inventory on dealership lots passes through wholesale auto auctions where vehicles are sold without buyer inspection rights and where a range of conditions including prior flood damage structural repair and mechanical issues are disclosed only to auction insiders through coded announcements. Dealerships purchasing at auction acquire vehicles at prices that reflect known issues that are then not disclosed to retail buyers who have no visibility into the auction transaction history. Vehicles sourced from insurance write-off pools rental fleets or fleet disposal programs carry specific use histories that affect longevity and reliability in ways that are not always reflected in standard history reports. Asking directly and specifically about a vehicle’s sourcing history and acquisition pathway is a question dealerships are rarely prepared for uninformed buyers to ask.

Financing Markup

When a dealership arranges financing through a bank or lender on a buyer’s behalf the interest rate presented to the buyer is frequently higher than the rate the lender actually approved with the markup representing direct profit to the dealership known in the industry as dealer reserve. A buyer approved by a lender at four percent may be presented with a six percent rate with the two percent difference generating thousands of dollars in additional revenue over the loan term without the buyer’s knowledge. Obtaining pre-approved financing from a bank or credit union before visiting the dealership establishes a competing rate that eliminates the markup opportunity and gives the buyer leverage to negotiate on the vehicle price as a separate variable. Dealerships that offer to beat an existing pre-approval are still frequently capable of profit through other transaction elements.

Pressure Through Scarcity

Claims that another buyer is interested in the same vehicle that the price will increase tomorrow or that the current offer expires at the end of the day are pressure tactics designed to accelerate buyer decision-making and prevent the comparison shopping and independent research that consistently leads to better outcomes. Genuine scarcity occasionally exists in the used vehicle market but the frequency with which these claims appear in sales conversations vastly exceeds any authentic inventory dynamic. A buyer who is willing to walk away from a vehicle under fabricated urgency pressure and return the following day or week will find in the overwhelming majority of cases that the vehicle is still available at a negotiable price. The willingness to leave is the single most effective negotiating tool available to any used car buyer.

Paint and Bodywork Concealment

Freshly detailed and professionally photographed vehicles conceal a significant amount of paint and bodywork information that is only visible under specific lighting conditions including direct sunlight oblique artificial light or the beam of a focused flashlight along panel surfaces. Overspray on rubber trim uneven panel gaps inconsistent paint texture between adjacent panels and color variance under different lighting angles are all indicators of prior bodywork that professional detailing is specifically effective at minimizing for lot presentation. Inspecting a vehicle outdoors in direct sunlight and running a hand along every panel surface to feel for texture inconsistencies reveals information that indoor showroom lighting is designed to suppress. A paint thickness gauge available inexpensively provides objective measurement of whether additional layers of paint consistent with prior repair exist on any given panel.

Warranty Limitations

Extended warranties sold by dealerships whether dealer-branded or through a third-party administrator contain exclusions conditions and claim processes that buyers rarely read in full before purchase and which frequently result in denied claims for repairs that buyers assumed were covered. Common exclusion categories include pre-existing conditions that the contract defines broadly wear and tear items that overlap with mechanical components and requirements for maintenance documentation that buyers cannot retrospectively produce. The claims process for many dealer-sold warranties involves dealership authorization steps and administrator approval delays that make the coverage practically less accessible than its marketing implies. Reading the full warranty contract including all exclusions before agreeing to purchase it rather than accepting a summary description is the only reliable way to evaluate whether the coverage justifies the cost.

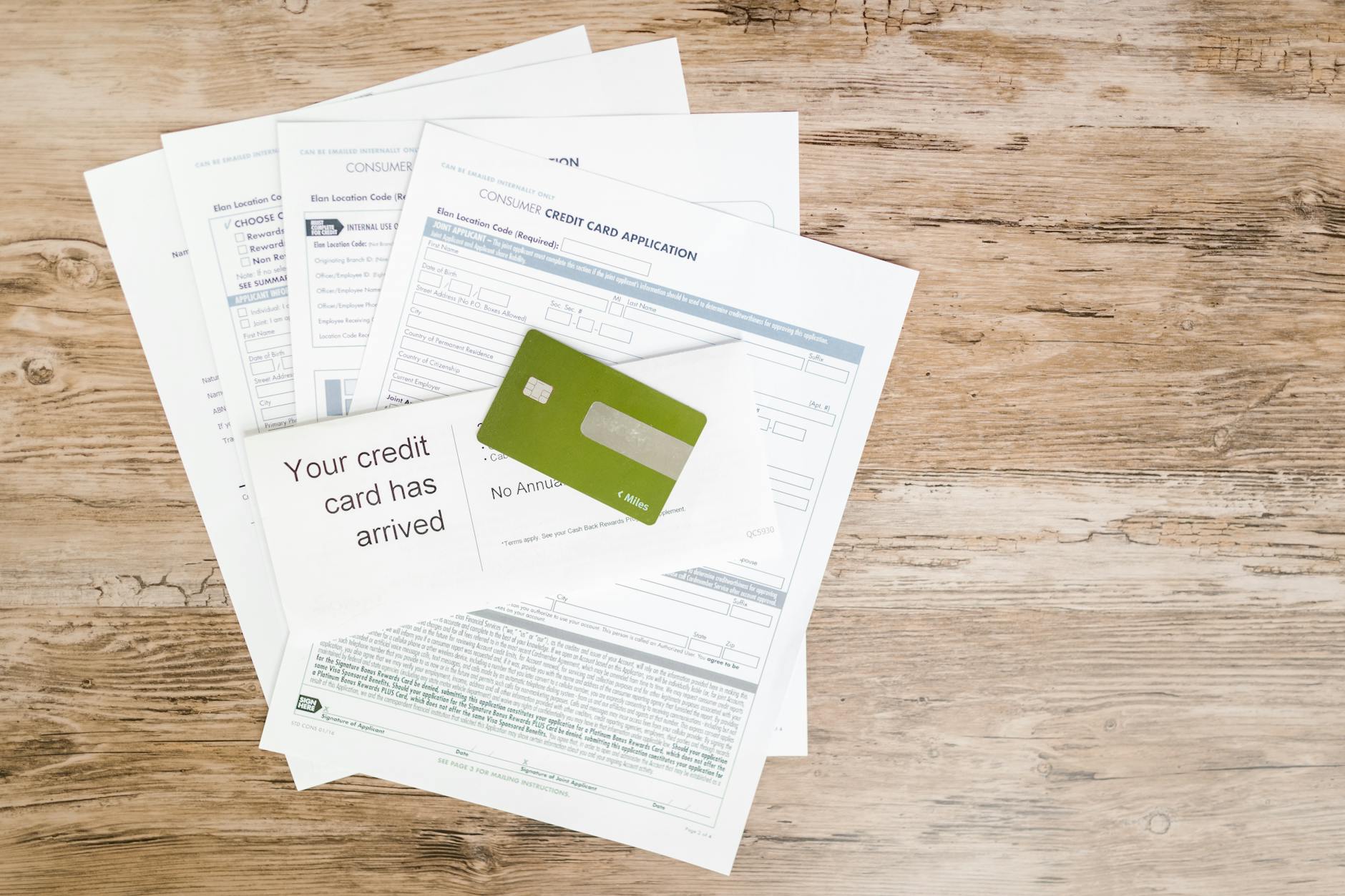

Credit Application Sharing

When a buyer submits a credit application at a dealership that application is in many cases shared with multiple lenders simultaneously generating several hard credit inquiries rather than a single one as buyers typically assume. While credit scoring models do provide a window within which multiple auto loan inquiries are treated as a single inquiry for scoring purposes the practice means that a buyer’s financial profile is distributed more broadly than most people realize or consent to with full understanding. The personal financial data submitted in a dealership credit application is also retained by the dealership independently of the financing outcome and represents a significant data asset that the buyer has no ongoing visibility into. Understanding what is being authorized in the credit application process before signing is a consumer right that sales staff are not incentivized to explain proactively.

Lease Buyout Inflation

Vehicles coming off lease that are purchased by the dealership rather than the original lessee for resale carry a book value that the dealership acquired at residual lease price but which is frequently retailed at a significant markup that the buyer has no visibility into. The lack of transaction transparency around how and at what price a vehicle was acquired by the dealership means that buyers cannot easily evaluate the margin being extracted from them in the way they might research manufacturer invoice pricing on a new vehicle. Researching the market value of a specific off-lease model against its posted price using multiple valuation tools provides the comparative data needed to negotiate from an informed position. The off-lease vehicle category is among the most systematically overpriced segments of the used market precisely because buyers tend to associate lease return status with quality certification.

Title Delay Tactics

Dealerships that delay delivering a clean title to the buyer after a cash or financed purchase are in some cases using the float period to resolve title issues that should have been resolved before the sale was completed. Issues including prior liens that have not been formally released title errors from previous ownership or administrative issues with the dealership’s own floor plan financing can all create delays that the buyer funds unknowingly by taking possession of a vehicle whose title status is not yet clean. Understanding the legally required timeline for title delivery in your jurisdiction and holding the dealership to that timeline explicitly from the point of sale prevents the most common forms of title delay exploitation. Any dealership that cannot commit to a specific title delivery date at the point of sale is communicating that a title issue exists whether or not it is disclosed.

As-Is Documentation

The as-is designation on a used vehicle purchase contract eliminates virtually all implied warranties of merchantability and fitness that would otherwise attach to the sale under consumer protection law in many jurisdictions. Buyers who sign an as-is contract and subsequently discover mechanical failures that the dealership was aware of at the point of sale have significantly narrowed legal recourse compared to buyers who purchased under implied warranty protections. The as-is checkbox is frequently buried within standard contract language and initialed without buyers understanding the legal weight of what they are waiving. Asking explicitly before signing whether the vehicle is being sold as-is and what that designation means for post-sale recourse is a question every buyer should put directly to the finance manager.

Demo Mode Manipulation

Allowing a buyer to take a vehicle for an extended test drive or an overnight demonstration is a strategy that leverages the psychological principle of the endowment effect whereby people place higher value on things they have temporarily experienced as their own. The longer a buyer spends with a vehicle the more emotionally attached they become and the more willing they are to accept unfavorable terms to complete the acquisition. Overnight demos are particularly effective at generating this attachment and are offered most consistently on vehicles with higher margins or slower sales velocity where the dealership’s motivation to close at almost any terms is highest. Recognizing that an extended demo is a sales tool rather than a service allows buyers to enjoy the experience while maintaining the emotional detachment needed for rational negotiation.

GAP Insurance Markup

Guaranteed asset protection insurance which covers the difference between what a buyer owes on a loan and what an insurer pays in the event of a total loss is a genuinely useful product in certain financing situations but is sold by dealership finance offices at markups of two to four times the price available directly through independent insurers or the buyer’s existing auto insurance provider. The finance office presentation of GAP as an exclusive or specialized product is a framing designed to prevent buyers from comparison shopping which takes less than ten minutes with a phone call to an existing insurer. Buyers who genuinely need GAP coverage based on their loan-to-value ratio should purchase it separately before or after the dealership transaction rather than accepting the finance office version. The premium difference between a dealer-sold and independently purchased GAP policy routinely runs into hundreds of dollars.

Hidden Reconditioning Fees

A reconditioning or make-ready fee appearing on a purchase contract represents a charge for the basic preparation work including cleaning mechanical safety checks and cosmetic touch-ups that the dealership performs on every vehicle before placing it on the lot and which is already factored into the retail asking price. Charging this fee as a separate line item on top of the agreed purchase price is double-billing for the same preparation cost and is a practice that buyers who notice it frequently succeed in having removed entirely through direct objection. The existence of the fee relies on buyers assuming it represents a legitimate additional service rather than recognizing it as a repackaged component of the standard retail margin. Scrutinizing every line item on the purchase contract before signing with specific attention to preparation and reconditioning entries protects against this consistent practice.

Negotiation Theater

The salesperson leaving the negotiating table to consult with a manager is a choreographed element of the sales process rather than a genuine consultation and the delay is specifically engineered to increase buyer anxiety and commitment to the deal as time passes. The back-and-forth between salesperson and manager creates the impression of a contested negotiation happening on the buyer’s behalf when in most cases the parameters of acceptable deal terms are communicated through a brief and informal exchange with no meaningful advocacy occurring. Buyers who recognize this theater are less susceptible to the urgency and gratitude that the returning salesperson attempts to generate when presenting what is framed as a hard-won concession. Conducting negotiations via email before visiting the dealership removes this dynamic entirely by forcing all counteroffers into writing where theater is impossible.

Lemon Law Loopholes

Vehicles that have been repurchased by manufacturers under lemon law statutes following repeated unresolved defects are legally required to carry disclosure in some jurisdictions but the disclosure requirements vary significantly and the vehicles frequently re-enter the used market through channels that place disclosure responsibility at a point in the ownership chain distant from the retail buyer. A buyer purchasing what appears to be a low-mileage clean-history vehicle may be acquiring a manufacturer buyback whose defect history is legally disclosed somewhere in the transaction chain but is never practically communicated at the point of retail sale. Running a VIN check specifically for manufacturer buyback status through resources including the National Highway Traffic Safety Administration database adds a layer of investigation that standard history reports do not consistently provide. Dealerships are not universally required to volunteer buyback history and will rarely do so unprompted.

Flood Vehicle Infiltration

Vehicles that have been submerged in flood water present long-term electrical corrosion mechanical contamination and mold-related health risks that manifest progressively over months and years after purchase and which can be concealed through professional cleaning and drying for long enough to complete a retail transaction. Flood-affected vehicles enter the used market in significant volumes following major weather events and are distributed through auction and wholesale channels that move them geographically away from their region of damage before retail sale. Inspection indicators including musty odor under carpet and in the trunk water staining on seatbelt webbing rust on non-weather-exposed metal components and mud residue in seams and cavities provide physical evidence that professional cleaning cannot consistently eliminate. An independent mechanic inspection that specifically includes checking for flood indicators is the most reliable protection available to a retail buyer with no auction access.

Invoice Price Misconception

The manufacturer invoice price which represents what the dealership paid for a new vehicle has a less direct equivalent in the used vehicle market but buyers frequently apply the same framework incorrectly by assuming that the book value or trade-in value represents the dealership’s acquisition cost for a used vehicle. In reality the gap between what a dealership pays for a used vehicle through trade-in purchase or auction and its retail asking price is often significantly larger than the equivalent margin on a new vehicle making the used vehicle transaction frequently more profitable per unit for the dealership. Understanding that standard valuation tools show retail and trade-in ranges rather than dealership acquisition cost helps calibrate realistic expectations for what constitutes a fair negotiation outcome. Researching recent actual transaction prices for specific vehicles through resources that aggregate real sales data provides a more accurate market picture than book value ranges alone.

Inspection Resistance

A dealership that discourages delays or creates friction around a buyer’s request to have a vehicle independently inspected by a mechanic of their choosing is communicating through that resistance that an inspection would reveal information unfavorable to the sale. The right to have a prospective purchase independently inspected before commitment is fundamental and a legitimate dealership selling a vehicle in the condition it represents has no rational incentive to obstruct that process. Buyers who encounter any form of inspection resistance should treat it as a significant signal about the vehicle’s undisclosed condition and escalate the inspection requirement rather than accepting reassurances that substitute for it. Walking away from any dealership that refuses independent inspection access is consistently the correct decision regardless of how attractive the vehicle or price appears.

Dealer Plate Concealment

Vehicles on a dealership lot that carry dealer plates rather than the prior owner’s registration may have an ownership and usage history that differs from what the posted vehicle description implies including prior use as dealership loaner vehicles test drive fleet vehicles or vehicles that have been on the lot and returned or exchanged. The absence of prior registration in the vehicle history does not indicate a new vehicle in the consumer sense and a car that has accumulated miles under dealer plates may carry wear that its history report significantly underrepresents. Asking directly about a vehicle’s prior use including whether it served any function as a dealership operational vehicle before being listed for retail sale forces the disclosure conversation that would not otherwise occur. Mileage and condition that feel inconsistent with a vehicle’s represented history often originate in this undisclosed prior use category.

Software and Data Retention

Modern vehicles store significant personal data including navigation history paired phone contacts call logs and location data from prior owners that dealerships are not consistently required to clear before resale and which buyers rarely think to investigate. The connected vehicle ecosystem means that a used vehicle may still be linked to prior owner accounts on manufacturer apps and connected services giving those prior owners potential ongoing access to location data and vehicle status information. Performing a factory reset of all infotainment and connected systems immediately upon taking possession and registering all connected vehicle services under the new owner’s credentials are essential steps that no dealership will proactively guide a buyer through. The data privacy dimension of a used vehicle purchase has grown significantly with each generation of connected vehicle technology and remains almost entirely absent from standard dealership disclosure conversations.

Holdback Exploitation

New vehicle dealerships receive a holdback payment from the manufacturer representing a percentage of the invoice or MSRP that is paid back to the dealership after the vehicle is sold creating a profit buffer that exists even when a salesperson claims to be selling at or below invoice. While holdback is a new vehicle market mechanism its existence means that dealer claims of zero profit or below-cost selling on new vehicles are almost categorically false and understanding this undermines the credibility of the no-margin framing that dealerships frequently use to justify resistance to further price negotiation. Buyers who understand holdback recognize that invoice price is not the floor of dealership profitability and that the true cost basis of the transaction is lower than any document provided during negotiation will reflect. This knowledge does not eliminate dealership profit which is legitimate but it does recalibrate the buyer’s sense of what a fair negotiation outcome looks like.

Service History Fabrication

Printed or presented service records that accompany a used vehicle are not always verified through the service department that supposedly produced them and instances of fabricated or altered service documentation are a documented form of fraud in the used vehicle market. Cross-referencing presented service records against the service department’s actual database by contacting the shop directly provides verification that the documents themselves cannot. Discrepancies between mileage figures in service records and the vehicle’s current odometer wear profile or history report entries are the most common indicators of documentation that has been altered or manufactured. Treating service records as a starting point for verification rather than as confirmed documentation is the appropriate level of skepticism for any high-value used vehicle purchase.

If any of these dealership tactics have caught you off guard or if you have your own hard-won experience navigating a used car purchase share your story in the comments.